AnswersPublished33 sources

Inside the PBOC's Yuan Strategy: What the Widening Fixing Gap Means and Why AI Predictions Fall Short

The widening gap between the PBOC's daily USD/CNY fixing and market estimates is a deliberate policy tool — a negative countercyclical factor — used to slow the yuan's roughly 6% appreciation and protect export compet... Currency traders are applying transformer based AI models, including NTU research on automated f...

AI Prompt

openai.comCreate a landscape editorial hero image for this Studio Global article: What explains the growing gap between the People's Bank of China's daily USD/CNY central parity rate and market expectations, how are curren. Article summary: The yuan has strengthened roughly 6% over the past twelve months to about 6.76 per dollar [7], and the PBOC is actively managing the pace of that rise. The widening gap between the daily fixing and market expectations is. Topic tags: general, government, general web, academic. Reference image context from search candidates: Reference image 1: visual subject "The graph illustrates the People's Bank of China's central parity rate for USD/CNY compared to market expectations from late January 2024 to early June 2025, with green representin" Reference image 2: visual subject "A weekly candlestick chart shows the USD/CNY exchange rate from early 2023 to mid-2026, hig

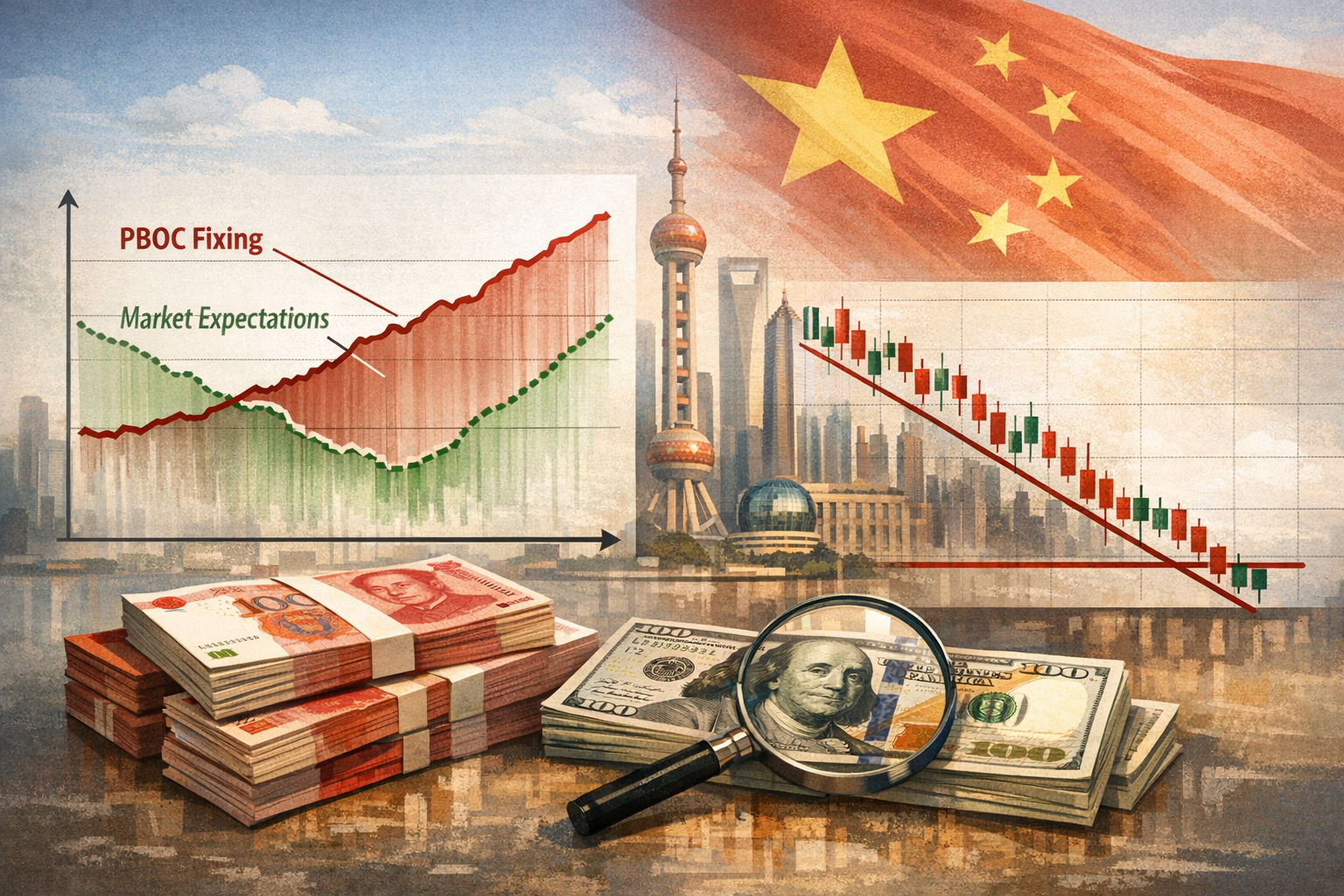

The Chinese yuan has rallied from 7.35 per dollar in April 2025 to roughly 6.76, an appreciation of about 8% . What appears as an erratic data series — a daily central parity rate that increasingly deviates from consensus forecasts — is in fact a deliberate monetary tool. The People's Bank of China (PBOC) is actively engineering a controlled appreciation, using a widening fixing gap as a valve to release pressure without igniting a speculative surge. For currency traders, this has turned the daily fixing into a high-stakes prediction target where artificial intelligence is now a frontline tool. Here is how the gap works, how AI is being deployed to narrow it, and why a perfect prediction remains out of reach.

The mechanics of the widening gap

The PBOC sets the daily USD/CNY central parity rate — known as the fixing — every weekday at 09:15 Beijing time, which then establishes a ±2% trading band for the session . The formula has three components: the previous day's closing spot rate, an adjustment for overnight moves in a trade-weighted currency basket, and a countercyclical factor (CCF). The CCF is a discretionary knob the central bank can turn to lean against market momentum

.

Since December 2025, that knob has been turned to negative, meaning the PBOC is systematically setting fixings weaker than the mechanical formula would produce on its own — a direct effort to decelerate yuan appreciation . The numbers show the policy in action:

- April 22, 2026: Fixing at 6.8635 vs. market estimate of 6.8233 — a 0.59% deviation

.

- May 15, 2026: Fixing at 6.8415 vs. Reuters estimate of 6.7976 — a gap of roughly 440 pips

.

- May 18, 2026: Fixing at 6.8435 vs. estimate of 6.8086

.

The motivation is a record-breaking trade machine. China's exports reached $3.8 trillion in 2025, producing a $1.2 trillion surplus . An uncontrolled yuan surge would erode export price advantages precisely when domestic deflationary pressures are already suppressing consumer confidence

. The PBOC is walking a tightrope: permit gradual appreciation — up to 8% already — while preventing the kind of fast, one-directional moves that invite speculative hot-money inflows and destabilize the currency

.

The negative CCF is a deliberate half-step: it signals that further appreciation is acceptable, but at the central bank's chosen pace, not the market's .

How traders are using AI to reverse-engineer the fix

For traders, the daily fixing is the single most important number in the Asian session. Being on the wrong side of a surprise fixing can erase weeks of gains. This has driven a practical arms race in prediction, with transformer-based deep learning models — the same architecture powering large language models — now at the center of effort.

A 2024 study by Lu Zhao and Wei Qi Yan found that transformer-based models "considerably surpass" LSTM and other legacy neural networks in currency exchange rate prediction, particularly during periods of heightened volatility . More specifically, a Temporal Fusion Transformer (TFT) achieved an R² of up to 0.94 in exchange rate forecasting in independent testing, with the addition of volatility indices like the VIX further improving accuracy

.

The most directly relevant academic work comes from a 2024 collaboration between Nanyang Technological University's College of Computing and Data Science, the Central University of Finance and Economics, and the Chinese Academy of Sciences. The researchers challenged the standard approach of manually constructing financial factors to predict the PBOC fixing and instead proposed an end-to-end model, the Intraday Risk Factor Transformer (IRFT), to extract latent predictive features directly from raw market data — essentially, automating the search for the hidden countercyclical factor .

Separate work at NTU has extended these lines of inquiry. One study applied deep learning to forex time-series prediction and used counterfactual explanations to make the model's reasoning interpretable . The "DeepForex" project on GitHub, affiliated with an NTU researcher, combined a Transformer price-prediction model with a Deep Q-Network (DQN) reinforcement learning agent to execute automated trades — integrating prediction with action

.

Institutional interest, notably from the Bank for International Settlements (BIS), has also validated the approach. A BIS working paper combined recurrent neural networks with large language models to forecast and explain currency market dysfunction 60 business days in advance, underscoring that central banks themselves are studying these methods .

In practical trading terms, the workflow looks like this:

- Known components (the prior close and overnight basket movements) are fed as structured inputs.

- The hidden CCF is treated as an unobserved latent variable — the model's central learning objective is to infer it from historical patterns of fixing behavior.

- Outputs inform pre-fixing position-taking, with positioning completed before the 09:15 Beijing time announcement releases the official number

.

The irreducible limit: policy is not a statistical process

The problem with predicting the PBOC fixing is not that the data is noisy. It is that the signal itself — decisions about the countercyclical factor — originates in an opaque, multi-objective political-economic calculus that leaves no clean numerical footprint.

First, the CCF is a signaling mechanism. When the PBOC sets a fixing 440 pips weaker than consensus, that gap is the message. It communicates to markets, trading partners, and domestic exporters that the central bank will not tolerate a fast appreciation, even if the mechanical formula would produce one . No historical price series contains this morning's political intention.

Second, the PBOC's policy preferences are non-stationary. From mid-2023 through late 2024, the CCF was deployed to resist depreciation, at times producing fixings dramatically stronger than market estimates to cap dollar strength . Since December 2025, it has flipped to resisting appreciation

. A model trained on the depreciation-era regime would be structurally wrong in the current environment — and the shift occurred with no explicit announcement, visible only in the post-hoc inferred CCF.

Third, the PBOC can change its stance overnight. A trade negotiation development, a Politburo meeting outcome, or a shift in domestic economic priority can alter the acceptable pace of appreciation before any market data reflects it.

In backtests, AI models can learn historical PBOC reaction functions and achieve high R² values, but the residual error is not noise — it is discretion. The models measure what can be measured; the CCF, by construction, measures what the central bank wants at that specific moment. When the gap widens, the gap is the output. The political input that produces it remains unobservable to any purely data-driven system.

Studio Global AI

Search, cite, and publish your own answer

Use this topic as a starting point for a fresh source-backed answer, then compare citations before you share it.

People also ask

What is the short answer to "Inside the PBOC's Yuan Strategy: What the Widening Fixing Gap Means and Why AI Predictions Fall Short"?

The widening gap between the PBOC's daily USD/CNY fixing and market estimates is a deliberate policy tool — a negative countercyclical factor — used to slow the yuan's roughly 6% appreciation and protect export compet...

What are the key points to validate first?

The widening gap between the PBOC's daily USD/CNY fixing and market estimates is a deliberate policy tool — a negative countercyclical factor — used to slow the yuan's roughly 6% appreciation and protect export compet... Currency traders are applying transformer based AI models, including NTU research on automated financial factor extraction, to infer the hidden policy adjustment and position ahead of the daily 09:15 Beijing time anno...

What should I do next in practice?

The central bank's discretionary objectives — which can shift from resisting depreciation to resisting appreciation overnight — represent an irreducible political variable, meaning AI can narrow but not eliminate pred...

Sources

- caixinglobal.comAnalysis: Where Is the Strengthening Yuan Headed? - Caixin Global

- tradingeconomics.comChinese Yuan - Quote - Chart - Historical Data - News

- fxmacrodata.comCNY Managed Float and Emerging Market Contagion - FXMacroData

- mexc.comPBOC USD/CNY Reference Rate Adjustment

- think.ing.comING Think | PDF | CNY at a glance: A surprise post-US election outperformer

- think.ing.com[PDF] CNY at a glance: what next as the yuan moves below the critical ...

- caixinglobal.comOffshore Yuan Breaches 7.0 Per Dollar to Hit 15-Month High

- fazen.marketsPBOC Sets USD/CNY Mid-Point at 6.8635 | Fazen Markets

- vtmarkets.netPBOC sets weaker yuan fix, widening gap to estimates as traders ...

- vtmarketsglobal.comPBOC Sets Weaker USD/CNY Fix, Reinforcing Expectations of ...

- uscc.govChina Bulletin: February 4, 2026

- chathamhouse.orgChina's $1.2 trillion trade surplus will increase calls for a ...

- accio.comYuan Trend 2026: Key Insights for Global Sourcing

- tmgm.comThe Yuan Surges, Midpoint Fixing Hits a New Three-Year ...

- think.ing.comCNY at a glance: what next as the yuan moves below ...

- ijmrset.comInternational Journal of Multidisciplinary

- cerv.aut.ac.nzPrediction of Currency Exchange Rate Based on Transformer

- cerv.aut.ac.nzPrediction of Currency Exchange Rate Based on ...

- arxiv.orgarXiv:2408.01271v2 [cs.CE] 5 Aug 2024

- dr.ntu.edu.sgCounterfactual explanations for forex prediction using deep learning methods

- github.comGitHub - nantha42/DeepForex

- bis.org[PDF] Harnessing artificial intelligence for monitoring financial markets

- mnimarkets.comMNI: PBOC Restarts Counter-Cyclical Factor In Yuan Fix-Traders

- federalreserve.govForeign Exchange Rates - H.10 - May 26, 2026

- think.ing.com[PDF] Asia FX Talking: China delivers controlled CNY appreciation - ing think

- wise.comChinese yuan rmb to US dollars Exchange Rate History - Wise

- think.ing.comAsia FX Talking: China delivers controlled CNY appreciation - ing think

- think.ing.comCNY at a glance: what next as the yuan moves below the critical ...

- tradingeconomics.comOffshore Yuan Holds Gains - Trading Economics

- globaltimes.cnYuan hits 33-month high against US dollar - Global Times

- cfr.orgChina's Currency is Now Facing Substantial Appreciation ...

- poundsterlinglive.comU.S. Dollar-Chinese Yuan History: 2026

- mexc.comPBOC USD/CNY Reference Rate Reveals Strategic 96-Point Yuan ...