AnswersPublished16 sources

Jensen Huang: The Biggest Constraint on AI Right Now Is Memory

Jensen Huang said at Dell World that memory—especially high‑bandwidth memory (HBM)—is now the biggest supply constraint for AI systems, meaning the pace of Nvidia H200 and next‑generation AI deployments may be limited... HBM shortages affect how many advanced AI accelerators Nvidia can ship, shift power toward memor...

AI Prompt

openai.comCreate a landscape editorial hero image for this Studio Global article: What did Jensen Huang say at Dell World about memory being the biggest AI supply constraint, how does the high-bandwidth memory shortage aff. Article summary: Jensen Huang’s message at Dell World was that AI demand is no longer constrained mainly by GPUs alone; memory, especially high-bandwidth memory, is becoming the key supply bottleneck. That matters because HBM availabilit. Topic tags: general, general web, user generated. Reference image context from search candidates: Reference image 1: visual subject "* Jensen Huang Weighs In on a Prolonged Memory Shortage as the AI Boom Continues, With Bubble Fears Still Lingering. Nvidia CEO Jensen Huang Directly Flags an AI Memory Supply Crun" source context "Jensen Huang Weighs In on a Prolonged Memory Shortage as the ..." Reference image 2: visual subject "* Jensen Huang

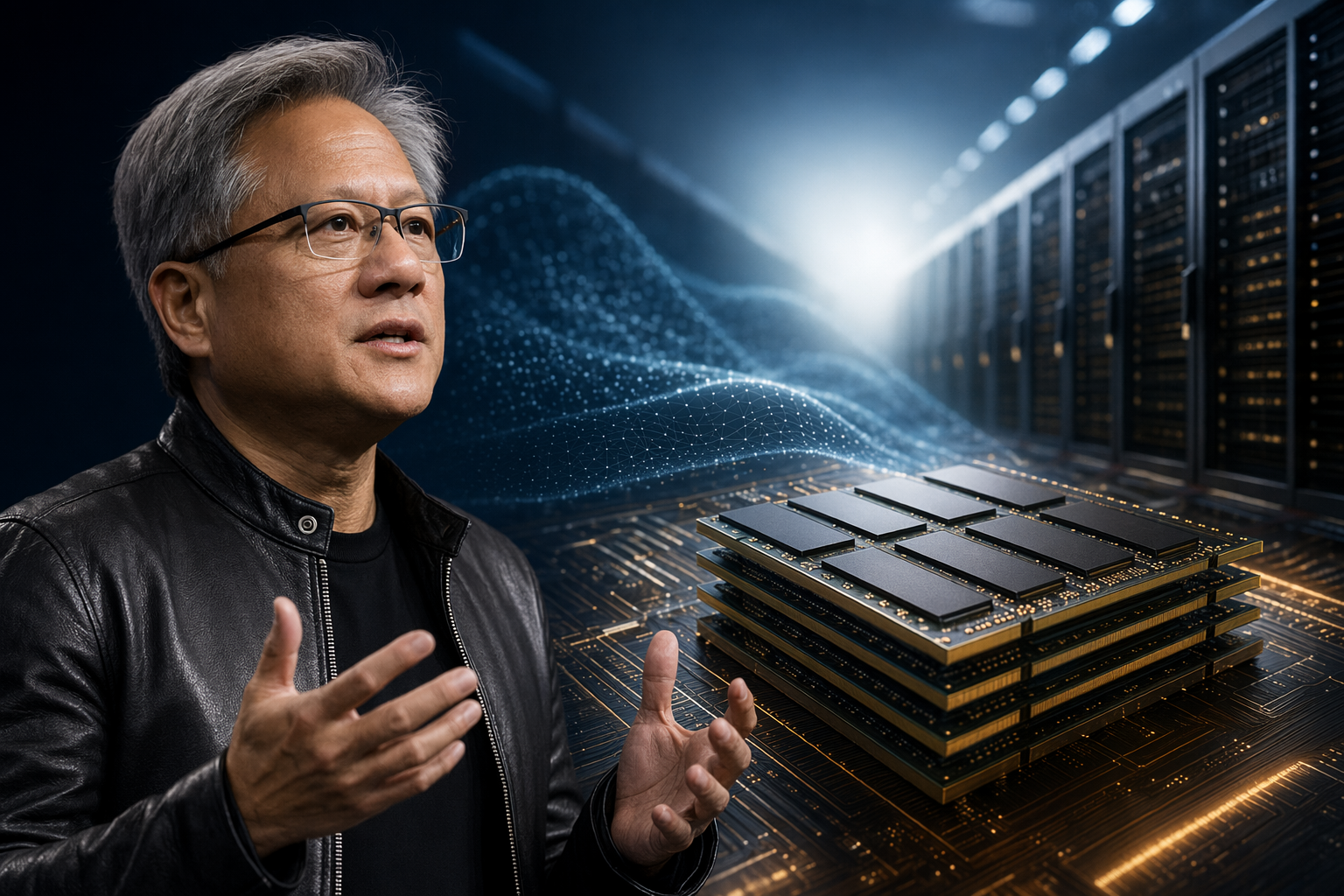

Artificial intelligence demand is still exploding—but according to Nvidia CEO Jensen Huang, the biggest constraint on the industry is no longer GPUs. It’s memory.

Speaking at Dell World in Las Vegas, Huang said that supply‑chain limits remain the biggest bottleneck for AI growth and pointed specifically to memory as a major constraint in the system stack. The comment highlights a shift in where the AI infrastructure race is hitting physical limits—and why investors are watching Nvidia’s supply chain closely ahead of its next earnings report.

Memory Has Become the New AI Bottleneck

Modern AI accelerators rely on high‑bandwidth memory (HBM)—a stacked DRAM technology designed to move enormous amounts of data between the GPU and memory chips at extremely high speed. Nvidia’s latest accelerators, including the H200 and systems based on its Blackwell architecture, depend heavily on these advanced memory stacks.

As AI models become larger and more complex, they require dramatically more memory bandwidth and capacity. Nvidia itself has warned that the future of AI performance will be shaped as much by memory capability as by raw compute power.

That creates a new constraint for the industry. Even if demand for GPUs is strong, Nvidia cannot ship a completed accelerator system without enough HBM attached. In practice, that means memory supply can directly cap how many AI chips reach customers.

The result: the AI boom is increasingly dependent on the output of a small group of memory manufacturers producing cutting‑edge HBM.

Why the HBM Shortage Matters for the Entire AI Industry

Studio Global AI

Search, cite, and publish your own answer

Use this topic as a starting point for a fresh source-backed answer, then compare citations before you share it.

People also ask

What is the short answer to "Jensen Huang: The Biggest Constraint on AI Right Now Is Memory"?

Jensen Huang said at Dell World that memory—especially high‑bandwidth memory (HBM)—is now the biggest supply constraint for AI systems, meaning the pace of Nvidia H200 and next‑generation AI deployments may be limited...

What are the key points to validate first?

Jensen Huang said at Dell World that memory—especially high‑bandwidth memory (HBM)—is now the biggest supply constraint for AI systems, meaning the pace of Nvidia H200 and next‑generation AI deployments may be limited... HBM shortages affect how many advanced AI accelerators Nvidia can ship, shift power toward memory suppliers, and could slow large AI data‑center deployments across the industry.

What should I do next in practice?

Huang also signaled optimism about China reopening to U.S. AI chips, but shipments of Nvidia’s H200 remain uncertain due to regulatory approvals and supply limits ahead of Nvidia’s May 20, 2026 earnings report.

Sources

- youtube.comNvidia CEO Huang Sees Demand for Memory Outpacing Capacity

- businesstimes.com.sgMemory shortage to hit Nvidia China approvals, US lawmaker says

- benzinga.comNvidia CEO Jensen Huang Says AI Memory Needs Are Rising ...

- thenews.com.pkNvidia CEO Jensen Huang hints China market may open to US chipmakers

- techloy.comJensen Huang Joins Trump in Beijing After Nvidia H200 Shipments ...