AnswersPublished21 sources

Why China Still Won’t Approve Russia’s Power of Siberia 2 Gas Pipeline

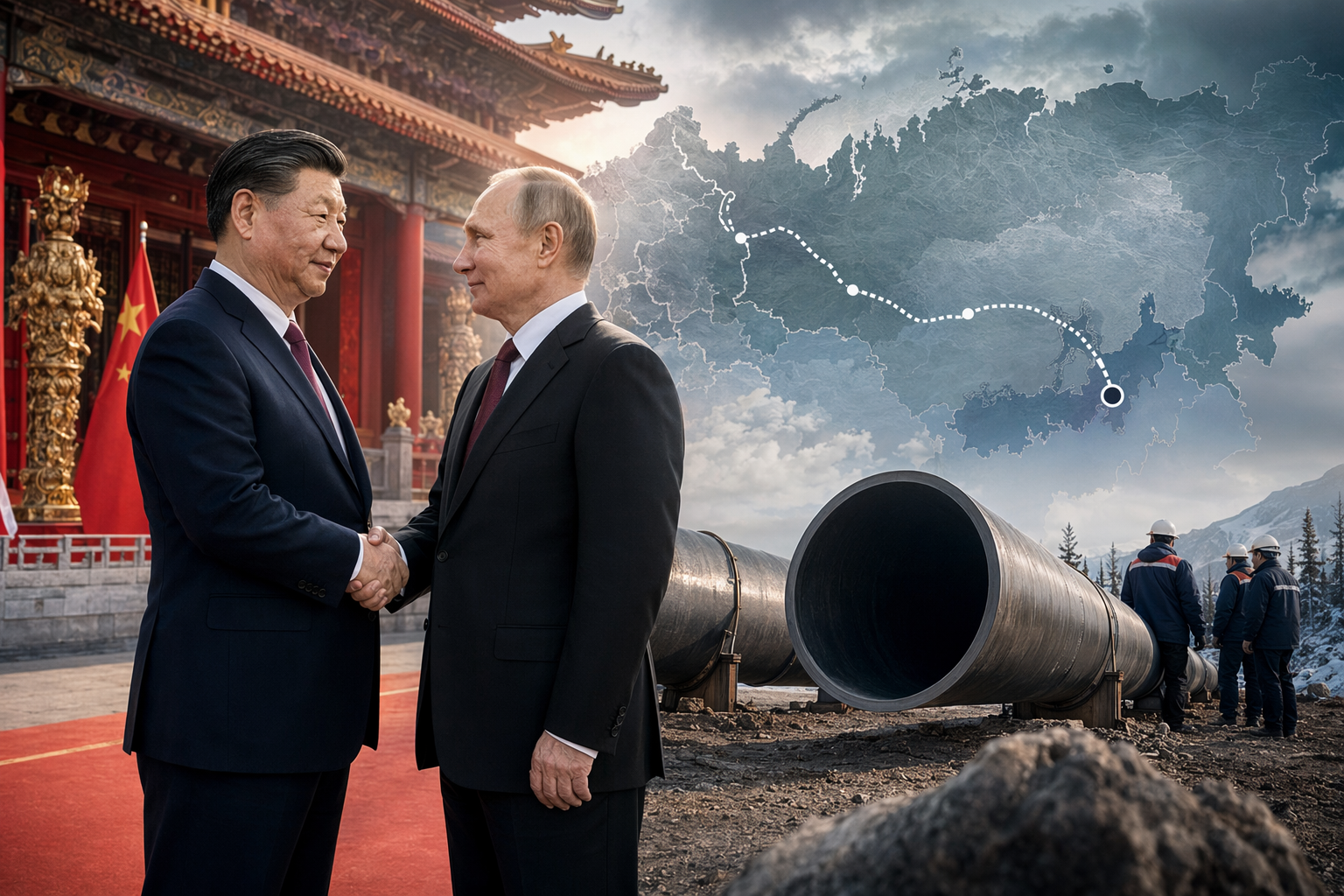

The May 2026 Xi–Putin summit in Beijing ended without a deal on the long‑planned Power of Siberia 2 gas pipeline. Russia needs the pipeline to redirect gas exports away from Europe after sanctions and the Ukraine war, while China can wait and negotiate for better terms.

AI Prompt

openai.comCreate a landscape editorial hero image for this Studio Global article: How did the recent Xi–Putin summit in Beijing affect plans for the Power of Siberia 2 gas pipeline, why has the project been delayed despite. Article summary: The Beijing summit did not unlock Power of Siberia 2: it produced political warmth and more talk of strategic cooperation, but no final gas-pipeline agreement. The delay reflects a hard economic reality: Russia needs the. Topic tags: general, general web, government. Reference image context from search candidates: Reference image 1: visual subject "Despite renewed focus on energy cooperation, there was still no clear timeline for the long-delayed, multibillion-dollar Power of Siberia 2 gas" source context "Xi-Putin meeting in Beijing: No clear timeline for stalled Power of Siberia 2 pipeline, Kremlin says" Reference image 2: visual subject "Xi-Putin meet in Bei

The latest summit between Chinese President Xi Jinping and Russian President Vladimir Putin in Beijing reinforced political alignment between the two countries—but it did not produce the breakthrough Russia wanted on the massive Power of Siberia 2 natural‑gas pipeline.

Despite years of negotiations and renewed urgency from Moscow, the leaders left the meeting without announcing a final agreement. The stalled project highlights a key reality in the China–Russia partnership: Russia needs the pipeline far more than China does, giving Beijing significant leverage in negotiations.

What the Beijing Summit Actually Achieved

Russia had hoped the meeting would unlock progress on the long‑delayed pipeline, which would send Siberian gas to China through Mongolia and potentially double Russia’s gas exports to the Chinese market.

Instead, the summit produced symbolic displays of strategic partnership and several cooperation agreements—but no public breakthrough on the pipeline itself.

Studio Global AI

Search, cite, and publish your own answer

Use this topic as a starting point for a fresh source-backed answer, then compare citations before you share it.

People also ask

What is the short answer to "Why China Still Won’t Approve Russia’s Power of Siberia 2 Gas Pipeline"?

The May 2026 Xi–Putin summit in Beijing ended without a deal on the long‑planned Power of Siberia 2 gas pipeline.

What are the key points to validate first?

The May 2026 Xi–Putin summit in Beijing ended without a deal on the long‑planned Power of Siberia 2 gas pipeline. Russia needs the pipeline to redirect gas exports away from Europe after sanctions and the Ukraine war, while China can wait and negotiate for better terms.

What should I do next in practice?

China’s diversified energy strategy—LNG imports, domestic gas, and massive renewable expansion—reduces the urgency to lock into decades‑long pipeline commitments.

Sources

- rferl.orgPutin Gets Show Of Unity, But No New Pipeline Deal In Beijing Summit

- businesstimes.com.sgPutin leaves Beijing after Xi meeting with little progress on key China-Russia gas pipeline project

- themoscowtimes.comHas the Iran War Sealed the Fate of Power of Siberia 2?

- internazionale.itXi and Putin unite to criticise US, but fail to clinch big gas deal

- pipeline-journal.netPutin Seeks to Jump-Start Major Russia-China Gas Pipeline Project Amid Middle East Turmoil